Markets closed sharply lower on Wednesday, with the S&P 500 falling 1.6% as investors continued rotating out of recent winners ahead of Friday’s record-breaking SpaceX IPO.

Index Performance

S&P 500: -1.60% → 7,267 Dow Jones: -1.87% → 49,918 Nasdaq 100: -1.98% → 28,508 Russell 2000: -1.10% → 2,835

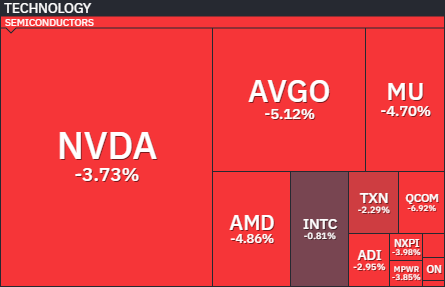

Semiconductors Take the Hardest Hit

The Philadelphia Semiconductor Index dropped 3.6%, with NVIDIA down 3.7%, Micron -4.7%, and Broadcom -5.1%. Super Micro Computer cratered 28% after announcing a $7 billion equity offering.

The sell-off in semis isn’t random. The thesis making the rounds is straightforward: investors are liquidating high-flying semi positions to raise cash for the SpaceX IPO — the largest in history. With OpenAI and Anthropic also potentially in the pipeline, the market is essentially bracing for a wave of mega-cap IPOs that could trigger significant portfolio rebalancing and draw capital away from recent winners.

Intel (INTC): A Pocket of Relative Strength

The Catalyst & Price Action

Intel has emerged as a notable outlier amidst the broader semiconductor sell-off. According to a June 8th report by The Information ( https://www.reuters.com/business/google-nvidia-consider-intel-backup-chip-manufacturer-information-reports-2026-06-08/), Google and Nvidia are evaluating Intel as a backup foundry partner, with Google reportedly placing an order for over 3 million TPUs. Buoyed by this news, the stock surged strongly above $110 on Monday, shaking off a 10%+ plunge from last week. While INTC couldn’t completely defy the sector-wide gravity, it is demonstrating striking relative strength compared to its peers.

Context: The Shakeout and Underperformance

To understand the current resilience, context is key. After previously touching $130, the stock subjected investors to a grueling pattern—consistently popping in the pre-market only to fade during regular trading hours. This frustrating price action effectively flushed out exhausted investors. Furthermore, Intel largely sat out the massive rally its peers enjoyed earlier, as the market was busy pricing in gradual CPU market share erosion driven by Nvidia and ARM’s entry into the space.

The Bottom Line for INTC

The narrative, however, appears to be shifting. The positive news surrounding its foundry business—heavily underpinned by U.S. government backing—is providing investors with a concrete thesis to hold and allocate capital, rather than using the recent bounce as an exit liquidity event.

Macro Data

May CPI came in at 0.5%, in line with expectations. The more encouraging number was core CPI at 0.2% — below the 0.3% forecast and well under April’s 0.4%. Disinflation is quietly continuing. The 10-year auction cleared at 4.538%, nearly matching the when-issued rate — a clean result with no surprises.

Rates, Dollar, Commodities

2Y yield: 4.145% ▲

10Y yield: 4.554% ▲

Dollar Index: 100.03 ▲

Gold: $4,094 ▼ (down sharply from $4,285)

WTI Crude: $91.85 ▲

Natural Gas: $3.178 ▲

Gold: The Cost of Holding Zero-Yield Assets

Gold’s sharp drop alongside rising yields tells a consistent story — risk appetite is shifting, not collapsing. With short-term rates climbing and the market increasingly pricing in further interest rate hikes by the Fed, the opportunity cost of holding non-yielding assets has surged. Consequently, the bullish catalyst for gold—which had recently enjoyed a massive run-up—is rapidly fading. This price action feels much more like a logical liquidity rotation toward yielding assets rather than a genuine fear-driven sell-off.

Crude Oil (WTI): Geopolitical Risk Premium and Diplomatic Theater

On the energy front, WTI crude’s recent strength is heavily driven by geopolitical risk premiums rather than structural demand. President Trump’s threat of a large-scale retaliation following the Iranian helicopter attack has reignited fears of a potential Strait of Hormuz blockade and a prolonged conflict.

However, the market is reading between the lines. Trump has concurrently stated that he is ready to negotiate at any time, suggesting his aggressive rhetoric is a calculated pressure tactic aimed at forcing a stalling Iran to the signing table. With the U.S. and Israel seemingly employing a diplomatic “good cop, bad cop” strategy, the current geopolitical premium is fragile. Therefore, rather than a sustained, one-way structural rally, we expect oil to be subjected to choppy, headline-driven volatility in the near term.

Bottom Line

The IPO pipeline is the story this week. Core CPI coming in soft was a genuine positive, but it got overshadowed by the sheer scale of capital demand hitting the market at once. Watch how semis behave post-SpaceX IPO — if the rotation thesis holds, there could be a meaningful bounce once the overhang clears.

Leave a Reply