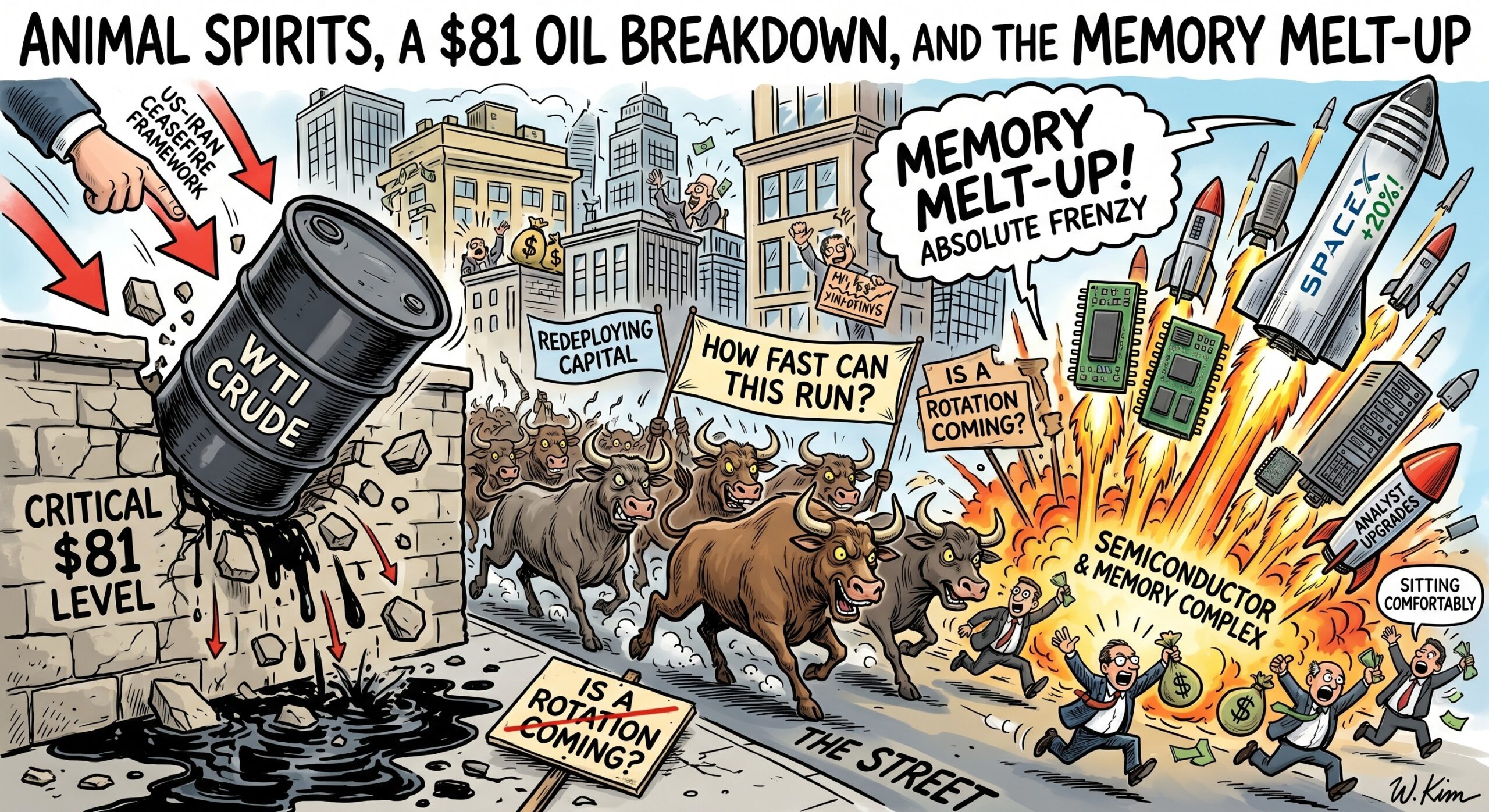

Today’s market recap for June 15, 2026 has the hallmarks of an animal-spirits day. With the US-Iran ceasefire framework shifting from rumor to reality, WTI crude broke below the critical $81 level, while a coordinated wave of analyst upgrades sent the semiconductor and memory complex into an absolute frenzy.

Capital that has been sitting comfortably on the sidelines is finally starting to redeploy. The conversation on the street has officially pivoted from “Is a rotation coming?” to “How fast can this run?”

Index Performance

Rates, Dollar, Commodities

This is an unusual but coherent triad. The market is simultaneously pricing in geopolitical de-escalation (oil dumping) and forward rate cuts (dollar slipping, gold catching a bid). Gold’s persistent strength, however, is a subtle tell: investors are treating the ceasefire as a massive relief, but they aren’t fully unhedged just yet.

The Iran Deal: From Speculation to Signatures

President Trump announced Sunday that the agreement with Iran is functionally “complete.” The MOU has reportedly been electronically signed, with a formal ceremony set for Friday in Switzerland. Crucially, the Strait of Hormuz is already partially reopened.

The market response was immediate and logical. Oil dumped on supply normalization. Equities rallied on the assumption that lower energy costs will drag inflation down with them. Keep an eye on airlines (DAL, UAL, AAL)—WTI breaking $81 drastically lowers jet fuel costs, directly expanding their operating margins.

Oil Under $81 — Airlines Take Flight

WTI breaking below $81 has second-order consequences that matter more than the headline number. Lower crude → lower jet fuel costs → airline margins improve. The sector traded accordingly. More broadly, the inflation narrative just got materially weaker, which feeds directly into the FOMC setup later this week.

SpaceX (SPCX) Day 2: Retail’s New Favorite Toy

Following Friday’s 19% IPO pop, SpaceX rallied another ~20% on Monday. The volume here isn’t being driven by institutions; it’s pure retail momentum. Net retail purchases of SpaceX exceeded $100 million for two consecutive sessions—matching the entire US market’s retail net buying from the prior week. This level of single-name concentration is historic, but it’s a dynamic that will warrant close monitoring as the initial lock-up windows eventually approach.

Memory Goes Vertical

The memory complex had one of its strongest single-day moves in recent memory:

- Micron: +10.84%

- Seagate: +9.43%

- Western Digital: +16.09%

The catalyst was a coordinated wave of analyst price target hikes on Micron:

- Allertia Capital: $650 → $1,600

- TD Cowen: $660 → $1,500

- RBC Capital: $525 → $1,200 — citing a tight supply environment that will sustain the DRAM up-cycle for 5–6 more quarters through the end of 2027

When three sell-side desks roughly double their PTs on the same day, it’s less about any single shop’s view and more about a thesis crystallizing across the street.

Broader semi names came along:

- ARM: +8.34%

- NVDA: +3.54%

- AVGO: +3.11%

- MRVL: +10.43%

- QCOM: +4.29%

- AMD: +6.98%

NVIDIA: Two Bull Calls Worth Reading

Two analyst notes on NVDA stood out today.

Melius Research: “AI agents are still in the early innings, and physical AI carries enormous untapped potential.” The bull case has shifted from training compute to inference and embodied AI — a multi-year runway argument rather than a near-term catalyst.

Lynx Equity went further with a contrarian framing: “The smarter way to invest in SpaceX is to invest in NVIDIA.” The logic being that the capex outlook for terafabs and xAI keeps moving higher, which broadens the beneficiary list well beyond NVDA itself:

- Semicap equipment: Lam Research, Applied Materials, ASML, KLA

- Semis: NVIDIA, Intel

- Memory: Micron, SanDisk

It’s a clean way to frame the AI capex thesis — the picks-and-shovels argument that’s quietly become the consensus trade.

AMD Adds a New Angle: The MEXT Acquisition

AMD (+6.98%) had its own catalyst: acquiring memory optimization specialist MEXT. The pitch—engineering flash memory to behave like DRAM—is a massive architectural swing. If AMD can execute this at scale, it directly addresses the severe memory bandwidth bottlenecks currently choking AI workloads.

The Anthropic Sideshow: Export Controls and a Lawsuit

A more complicated thread emerged around Anthropic. On Friday, the Trump administration announced export controls restricting foreign use of Anthropic’s Fable5 and Mythos5 models. The market reaction has been counterintuitive: rather than seeing this as a hit to US AI dominance, traders are reading it as a catalyst for non-US capex acceleration.

The logic runs as follows. If access to top US models becomes politically conditional, other countries will hedge by:

- Building out their own hardware capacity

- Constructing sovereign data centers

- Funding domestic frontier LLM development

Each of those lines flows back to the same beneficiaries — semicap, semis, memory — which is part of why today’s rally had such breadth across the chain.

The counter-view, voiced by several desks: the Anthropic-administration tension is noise, disconnected from the larger semiconductor and AI capex story. Both can be true.

Separately, Anthropic was hit with a class-action lawsuit today alleging that the company misled consumers about usage limits on its premium subscription tier. Not a market mover, but worth tracking as part of the regulatory backdrop building around frontier AI providers.

FOMC Wednesday: Warsh’s First Meeting

The dominant macro event this week is Kevin Warsh’s first FOMC meeting as chair. The setup is unusually tense.

What’s expected:

- A hold on the policy rate is the base case.

- December hike odds have fallen from 70% to 50% over the past two weeks.

- Consensus expects the statement to remove the dovish phrase “scope and timing of further adjustments” — a meaningful signaling shift.

The bull case: A dovish surprise sends the S&P up 10–15%, with AI names potentially doubling as MMF cash floods back in. This is the tail scenario but not a small tail.

The base case: A hawkish lean. Three regional Fed presidents — Hammack (Cleveland), Kashkari (Minneapolis), Logan (Dallas) — called for removing the accommodative bias back in April. Christopher Waller has separately argued for a “more neutral” stance. The June dot plot is expected to drop the single rate cut projected back in March.

The data backdrop supports the hawkish read. May CPI ran +0.5% m/m, +4.2% y/y. May PPI surged to +6.5% — a supply-chain inflation signal the Fed cannot ignore. And the labor market argument that supported the dovish case has weakened materially: three consecutive months of solid jobs data have undercut the “downside risk” narrative.

The Warsh wildcard: At a conference one year ago, Warsh said “dot plot forecasts have been terrible, and my own forecasts aren’t perfect either — I won’t issue them.” If he follows through and withdraws forward guidance entirely, the market will need to rebuild its rate path expectations from scratch. That’s either bullish (less anchoring) or destabilizing (more ambiguity) depending on how the press conference is read.

Bottom Line

Three forces are converging: geopolitical tensions are materially unwinding, sub-$81 oil is relieving inflation anxiety, and Wall Street is finally willing to underwrite massive valuation expansions for memory and semis.

The underlying fuel for all of this? The $8–9 trillion currently parked in Money Market Funds (MMFs). If Wednesday’s FOMC avoids a severe hawkish shock, that historic wall of cash has the green light to rotate back into equities.

Leave a Reply